Financial Services

-

Home Buyer Mortgage

First Time Buyer Guide to buying your own home.

-

Home Mover Mortgage

Elevate your move with our tailored Home Mover Mortgage for a smooth transition to your new dream home.

-

Home Owner Remortgage

Refinance with our Home Owner Remortgage for better rates, releasing equity, or funding improvements—empowering your homeownership journey.

-

Buy-to-Let Mortgage

Dive into property investment with our Buy-to-Let Mortgage, tailored for both seasoned investors and first-timers seeking to build a profitable portfolio.

-

Holiday Let Mortgage

Transform your vacation home investment dreams into reality with a Holiday Let Mortgage,

-

Green Mortgages

Green Mortgages 🌳 are a new type of mortgage that rewards you for making your home more energy efficient.

-

Bad Credit

Mortgages Adverse Credit Mortgages 📉 are for people with a poor credit history.

-

Private Medical Insurance

Cut NHS wait times with private medical care and private hospitals.

-

Life Insurance

Pay off your mortgage if you or your partner die.

-

Bridging Finance

Navigate property transitions seamlessly with our Bridging Finance, offering quick and secure solutions for your short-term financial needs.

-

Auction Finance

Secure your auction triumph with Auction Finance, providing the financial backing needed to confidently bid and acquire your desired property.

Mortgage Lenders can fund their mortgage lending in several ways. The two typical methods are:

- Customers Savings

- Government Funding Schemes

- Wholesale Markets

On top of charging a margin, lenders deciding what to charge also have to consider the cost of regulation, such as capital and liquidity requirements, default rates, administration, marketing expenses and SWAP rates.

( This Article was written in October 2022 following sharp increases in Mortgage Rates, Bank Base Rates and SWAP rates.)

- Customer Savings - A bank may offer people with savings a return on their money. They will add a percentage to this and lend it to Mortgage Borrowers, the Bank making their money on the difference between the two rates.

- Government Funding Schemes - Time-to-Time the Government will want to incentivise the banks to lend to certain types of borrowers. First Time Buyers are often the target of the UK Government, having schemes such as Help-to-Buy, which almost bypasses banks or other schemes such as the Mortgage Guarantee Scheme insuring banks.

- Wholesale Markets - Wholesale funding uses deposits and other liabilities from institutions such as the Bank of England, banks, pension funds, money market mutual funds and other financial intermediaries.

SWAP Rates

While a move in the Bank of England base rate is one event that could lead to changes in mortgage pricing, lenders regularly vary the rates they offer to the market and can move up or down.

The cost of borrowing in the 'Wholesale Market' is variable. The rates can go up and down. Banks need to insure against that fluctuation to offer you a fixed-rate mortgage. Lenders use swap rates, whereas the name suggests - two different parties swap interest rates. That means the price of a fixed-rate mortgage is based on the price at which they can insure themselves in the SWAP market.

The bank base rate has increased by 2.15% over the last year, going up from 0.10% to 2.25%. Except two-year swap rates have increased by 5.10% (from 0.44% to 5.56% as of 26 September).

SWAP rates reflect forecasts on what the Bank of England base rate may be soon, with widespread expectations that interest rates will continue to climb, directly impacting the swap market. Therefore impacting what fixed-rates mortgage lenders can offer you.

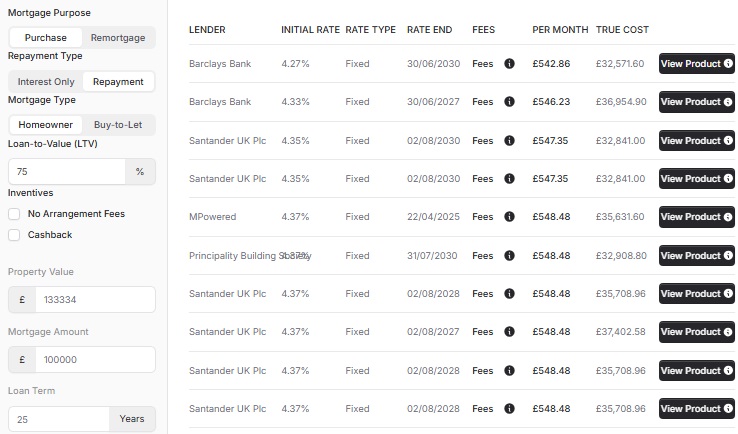

An Example of Pricing

( Quoted rates correct as of 11 October 2022)

The Bank Base Rate is at 2.25%, but The Mortgage Works (TMW) charges 5.14% (with a 3% fee) for a vanilla 2-Year Fixed 75% LTV Remortgage. Why?

You would think Lenders are making fantastic profits. They are charging almost double the Bank of England Base Rate.

Though that is not (exactly) the case. Mortgage Lenders need to insure themselves. Think of the Bank of England Base Rate as a Tracker, and Lenders want to offer you a Fixed Rate Mortgage.

To guarantee they profit and not lend you money that is profitable today but perhaps not next month. Lenders have to insure themselves with SWAP rates.

The SWAP market does take into account the Bank of England Base Rate. Though it's what the speculators *think* it will peak to in the future in 1 or 2 years.

The SONIA 2-Year SWAP rates are around 5% currently, though volatile.

This is why Tracker Mortgages remained in the market when many mortgage lenders pulled their Fixed Rate Mortgages. It's also the oddity of why sometimes 5-Year Fixes are cheaper than 2-Year Fixes.

This is a simplified explanation, but I hope it helps explain the high rates we are receiving now.

Why have mortgage rates increased, but Savings Rates have not?

The rate of return for savings has increased slightly, with The Times reporting, "Interest rates rise to 2.25%" on 27 September. The study said that only 26 easy access accounts (11.2%) had seen any increase in the rate paid following the 4 August Bank Base Rate rise. Sometimes banks will wait a while before making changes to savings rates – it may be several weeks or even longer. Though competition or lack of competition, including consumer apathy for searching for a better deal, many do not get around to switching.

Unfortunately, even if the latest increase is passed on in full, rising inflation – currently 9.4% and set to go higher – erodes the value of people's nest-egg cash.

In addition, Savings Rates won't increase to the extent of the Fixed Rate Mortgages as above. The cost of borrowing often does not drive the Mortgage Costs but the insurance (SWAP Rates).

Get in touch

We are your online mortgage broker, offering you the convenience of applying for a mortgage online. However, we understand that sometimes you may prefer to speak with a human - phone, email or in person.

- Phone number

- 01133 205 902

- hello@cyborg.finance

- Postal address

-

31 Bradford Chamber Business Park,

New Lane, Bradford, BD4 8BX

Looking for career in Mortgage Advice? View job openings.

We are authorised and regulated by the Financial Conduct Authority (No. 919921). The FCA does not regulate most Buy to Let mortgages.

Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

Cyborg Finance Limited is registered in England and Wales (No. 12131863) at Bradford Chamber, New Lane, Bradford, BD4 8BX