Financial Services

-

Home Buyer Mortgage

First Time Buyer Guide to buying your own home.

-

Home Mover Mortgage

Elevate your move with our tailored Home Mover Mortgage for a smooth transition to your new dream home.

-

Home Owner Remortgage

Refinance with our Home Owner Remortgage for better rates, releasing equity, or funding improvements—empowering your homeownership journey.

-

Buy-to-Let Mortgage

Dive into property investment with our Buy-to-Let Mortgage, tailored for both seasoned investors and first-timers seeking to build a profitable portfolio.

-

Holiday Let Mortgage

Transform your vacation home investment dreams into reality with a Holiday Let Mortgage,

-

Green Mortgages

Green Mortgages 🌳 are a new type of mortgage that rewards you for making your home more energy efficient.

-

Bad Credit

Mortgages Adverse Credit Mortgages 📉 are for people with a poor credit history.

-

Private Medical Insurance

Cut NHS wait times with private medical care and private hospitals.

-

Life Insurance

Pay off your mortgage if you or your partner die.

-

Bridging Finance

Navigate property transitions seamlessly with our Bridging Finance, offering quick and secure solutions for your short-term financial needs.

-

Auction Finance

Secure your auction triumph with Auction Finance, providing the financial backing needed to confidently bid and acquire your desired property.

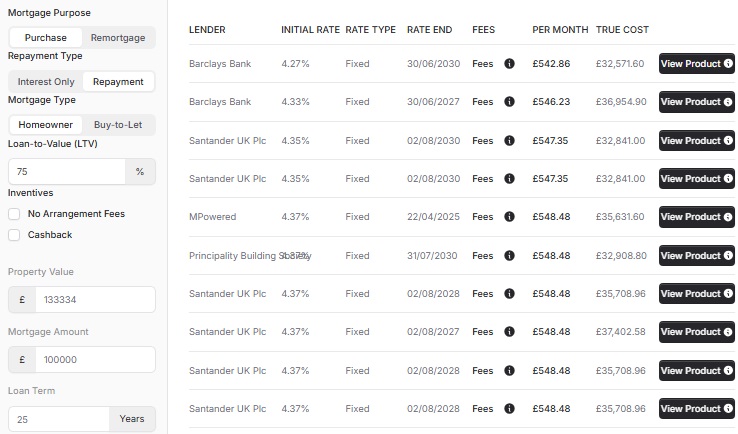

HMO Maximum Loan-to-Value (LTV)

HMO Mortgages are available with just 15% deposit

HMO Mortgages are available up to 85% LTV for Purchase or Remortgage. That's just a deposit of 15% of the property value. 85% LTV HMO Buy-to-Let mortgages are the highest LTV you can get as a property investor. Landlords looking to leverage prefer an 85% HMO Mortgage.

Lowest HMO 85% LTV Mortgage Rates

|

Rate

|

Fees

|

|

|---|---|---|

|

6.33%

2 Year Fixed

TBC

TBC

Fixed

at

6.33%

|

|

|

|

6.69%

5 Year Fixed

TBC

TBC

Fixed

at

6.69%

|

|

The mortgage products shown are for illustrative purposes only and were generated 55 minutes ago. Always consult an independent financial advisor before proceeding with any mortgage. The figures are based on a £117648 property value, a £100000 loan amount and £17648 deposit. Initial Fixed Rate on a interestOnly loan, and a 25-year mortgage term.

|

Rate

|

Fees

|

|

|---|---|---|

|

6.33%

2 Year Fixed

TBC

TBC

Fixed

at

6.33%

|

|

|

|

6.69%

5 Year Fixed

TBC

TBC

Fixed

at

6.69%

|

|

The mortgage products shown are for illustrative purposes only and were generated 55 minutes ago. Always consult an independent financial advisor before proceeding with any mortgage. The figures are based on a £117648 property value, a £100000 loan amount and £17648 deposit. Initial Fixed Rate on a interestOnly loan, and a 25-year mortgage term.

🔷What is an 85% LTV HMO Mortgage?

Loan to Value (LTV) is the mortgage amount percentage of the total value or purchase price. You can borrow up to 85% of the value of an HMO Property. As an example on a property worth £100,000. With an 85% LTV HMO Mortgage you can borrow up to £85,000. That means just a deposit or equity of £15,000. Mortgage Lenders consider 85% LTV as high risk giving us few options. The higher risk and fewer options are reflected in the mortgage rates and fees charged. Whilst 85% LTV HMO Mortgages are available. The maximum loan is still constrained by affordability, mainly the rent achievable.

🔷What are the benefits of 85% LTV HMO Mortgages?

HMO mortgages at 85 LTV are the highest property investors can obtain. Higher loan to value is not available for Buy-to-Let investors. On purchases, you can buy a property with very little deposit. Helping you to expand your portfolio. On remortgages, you can raise capital from your property. Enabling you to use funds elsewhere such as a renovation or expanding your portfolio.

🔷Can you borrow up to 85% LTV of the Property Value?

The affordability of a Buy-to-Let Mortgage is based on the rent that is achievable. It can be difficult for landlords to reach a rental stress test of 85%. Completing the mortgage on a Five Year Fix and/or Limited Company may open up more options. Our mortgage advisers will be able to guide you in this. For illustrative purposes only. On a mortgage of £170,000 with the Kensington Product, you would require £974 rent and £1090 from KRBS.

🔷85% LTV Mortgage Criteria

- Available for Houses in Multiple Occupation (HMOs)

- Available for Multi-Unit Blocks.

- Available for Limited Company Buy to Let.

- Available for Trading Companies.

- Available in England, Wales, Scotland and Northern Ireland.

- No Minimum Income.

- Interest Only or Repayment.

- Minimum 1 Year Landlord Experience Required

🔷Can you get 85% LTV HMO Mortgage in a limited company?

The products available are for Personal Name or in a Limited Company Buy-to-Let if purchasing in a Special Purpose Vehicle (SPV). Trading Companies differ.

🔷Are HMO Mortgages regulated?

HMO Mortgages are not regulated by the Financial Conduct Authority (FCA). These are classed as commercial mortgages.

🔷Talk to our HMO Mortgage Advisers

Get in touch

We are your online mortgage broker, offering you the convenience of applying for a mortgage online. However, we understand that sometimes you may prefer to speak with a human - phone, email or in person.

- Phone number

- 01133 205 902

- hello@cyborg.finance

- Postal address

-

31 Bradford Chamber Business Park,

New Lane, Bradford, BD4 8BX

Looking for career in Mortgage Advice? View job openings.

We are authorised and regulated by the Financial Conduct Authority (No. 919921). The FCA does not regulate most Buy to Let mortgages.

Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

Cyborg Finance Limited is registered in England and Wales (No. 12131863) at Bradford Chamber, New Lane, Bradford, BD4 8BX