Financial Services

-

Home Buyer Mortgage

First Time Buyer Guide to buying your own home.

-

Home Mover Mortgage

Elevate your move with our tailored Home Mover Mortgage for a smooth transition to your new dream home.

-

Home Owner Remortgage

Refinance with our Home Owner Remortgage for better rates, releasing equity, or funding improvements—empowering your homeownership journey.

-

Buy-to-Let Mortgage

Dive into property investment with our Buy-to-Let Mortgage, tailored for both seasoned investors and first-timers seeking to build a profitable portfolio.

-

Holiday Let Mortgage

Transform your vacation home investment dreams into reality with a Holiday Let Mortgage,

-

Green Mortgages

Green Mortgages 🌳 are a new type of mortgage that rewards you for making your home more energy efficient.

-

Bad Credit

Mortgages Adverse Credit Mortgages 📉 are for people with a poor credit history.

-

Private Medical Insurance

Cut NHS wait times with private medical care and private hospitals.

-

Life Insurance

Pay off your mortgage if you or your partner die.

-

Bridging Finance

Navigate property transitions seamlessly with our Bridging Finance, offering quick and secure solutions for your short-term financial needs.

-

Auction Finance

Secure your auction triumph with Auction Finance, providing the financial backing needed to confidently bid and acquire your desired property.

Labour promises 5% deposit mortgages

Freedom to Buy Scheme is claimed to help 80,000 First Time Buyers

Labour Leader Keir Starmer today unveiled the 'Freedom to Buy' scheme, a potential game-changer for first-time buyers. But what exactly is it, and how could it potentially benefit those looking to step onto the property ladder?

The Scheme already exists and has been in operation since 2021, when 5% of deposits disappeared post-pandemic, called "The Mortgage Guarantee Scheme". The Conservative Party scheme was due to end in 2025, but the Labour plan is to make it permanent.

The scheme will make taxpayers guarantors for borrowers unable to save up extensive deposits. The British public will cover some of the costs if a home is repossessed, which gives banks confidence to lend to higher-risk, low-deposit borrowers.

Labour pledged to help 80,000 young people, nearly double the 42,836 households the scheme helped in the two years and seven months the scheme has been running.

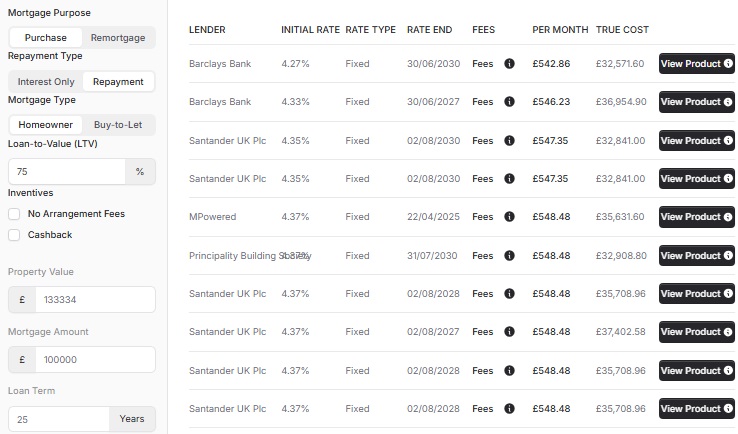

With over 19 Mortgage Lenders with 95% LTV Mortgages in the market and special offerings such as Accords £5k Deposit Mortgage, some may question the 'Freedom to Buy' scheme's need to be permanent.

Mortgage Experts, say..

Speaking to the Newspage news agency, Mortgage Specialists said

- "This policy is about as useful as a chocolate teapot" Lewis Shaw, Shaw Financial Services

- "Yet another scheme with no real substance. The existing mortgage guarantee offering has had limited take-up, and this will be no different," Katy Eanten.

- "Freedom to Buy looks great on the first read, but then you realise it’s actually been in place since 2021 and many lenders don’t use it anyway." Justin Moy, EHF Mortgages

- "The Mortgage Guarantee scheme has become almost obsolete with standard 5% deposit mortgages available" Stephen Perkins, Yellow Brick Mortgages

My view is that it's fine; every little helps first-time buyers and this is very little. The deposit is just one part of the puzzle. The reason for the scheme's low initial take-up is affordability. With the scheme currently being used on house prices worth £202,713, a homeowner must demonstrate that they can afford a £192,577 mortgage at today's 95% LTV rates of 5%- 7%. That's not easy to do.

Unless there are unannounced changes, I can not see the scheme reaching 80k people when it's taken nearly 3 years to reach 42k.

Reviewed and Approved 07 Jun 2024 by:

CEO, Cyborg Finance

Experienced Director with a demonstrated history of working in the financial services industry. Skilled in Business Planning, Portfolio Management, Business Relationship Management, and Business Development.

Get in touch

We are your online mortgage broker, offering you the convenience of applying for a mortgage online. However, we understand that sometimes you may prefer to speak with a human - phone, email or in person.

- Phone number

- 01133 205 902

- hello@cyborg.finance

- Postal address

-

31 Bradford Chamber Business Park,

New Lane, Bradford, BD4 8BX

Looking for career in Mortgage Advice? View job openings.

We are authorised and regulated by the Financial Conduct Authority (No. 919921). The FCA does not regulate most Buy to Let mortgages.

Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

Cyborg Finance Limited is registered in England and Wales (No. 12131863) at Bradford Chamber, New Lane, Bradford, BD4 8BX