Financial Services

-

Home Buyer Mortgage

First Time Buyer Guide to buying your own home.

-

Home Mover Mortgage

Elevate your move with our tailored Home Mover Mortgage for a smooth transition to your new dream home.

-

Home Owner Remortgage

Refinance with our Home Owner Remortgage for better rates, releasing equity, or funding improvements—empowering your homeownership journey.

-

Buy-to-Let Mortgage

Dive into property investment with our Buy-to-Let Mortgage, tailored for both seasoned investors and first-timers seeking to build a profitable portfolio.

-

Holiday Let Mortgage

Transform your vacation home investment dreams into reality with a Holiday Let Mortgage,

-

Green Mortgages

Green Mortgages 🌳 are a new type of mortgage that rewards you for making your home more energy efficient.

-

Bad Credit

Mortgages Adverse Credit Mortgages 📉 are for people with a poor credit history.

-

Private Medical Insurance

Cut NHS wait times with private medical care and private hospitals.

-

Life Insurance

Pay off your mortgage if you or your partner die.

-

Bridging Finance

Navigate property transitions seamlessly with our Bridging Finance, offering quick and secure solutions for your short-term financial needs.

-

Auction Finance

Secure your auction triumph with Auction Finance, providing the financial backing needed to confidently bid and acquire your desired property.

Bank of England Housing Update (February 2025)

Bank Base Rate CUT to 4.5% mortgages continue to fall and Housing is looking positive.

At its meeting on February 6th, 2025, the Monetary Policy Committee (MPC) voted by a majority of 7 to 2 to reduce the Bank Rate to 4.50% from 4.75%. However, Two members (Swati Dhingra and Catherine L Mann) preferred a larger reduction to 4.25%.

The market did anticipate this reduction, with mortgage lenders recently reducing mortgage rates and SWAP rates coming down. Almost all respondents to the Bank’s latest Market Participants Survey (MaPS) were expecting a 25 basis point reduction in Bank Rate at this MPC meeting.

The BoE is warning about Donald Trump various tariffs as a "rapidly evolving situation, which it would be monitoring closely".

The Bank Base Rate Reduction comes despite an anticipated rise in inflation (due to energy costs) as the MPC expects inflation to thereafter decrease back to the 2% target.

This is good news for

- Remortgaging Homeowners who need to remortgage as their initial rate ends.

- First Time Buyers trying to meet higher affordability requirements.

- Landlords hoping not to increase rents due to increased mortgage costs.

Inflation

In support of returning inflation to the 2% target, the BoE believes there has been disinflation in domestic prices and wages to reduce the Bank Rate to 4.5% at this meeting.

CPI inflation reached 2.5% in Q4 2024. Higher global energy costs and regulated price changes are expected to raise headline CPI inflation to 3.7% in Q3 2025 and later its anticipated to drop back to about 2%.

Bank of England on Housing

There are signs that housing market activity is picking up.

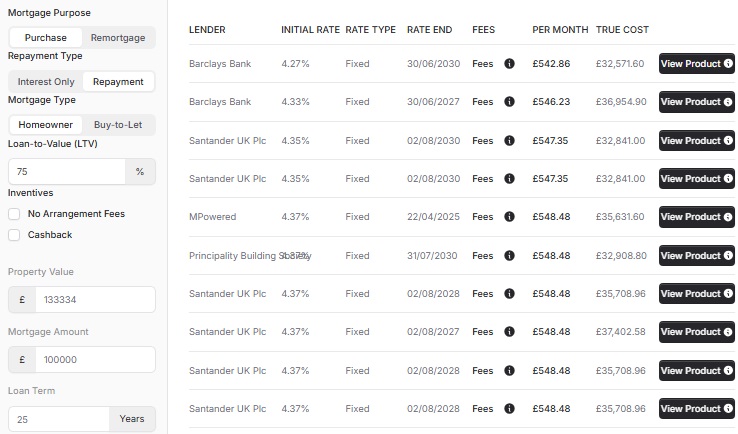

Pass-through to household loans appears to be progressing in line with historical experience with, as expected, interest rates for some products taking longer to fall than others. Average quoted rates on two-year fixed-rate mortgages with a loan to value (LTV) ratio of 75%, for example, have fallen by 55 basis points since May 2024. Since the November Report, average quoted rates on some fixed-term mortgages have increased slightly, reflecting the pick-up in the relevant OIS rates since September.

Past increases in mortgage rates are expected to result in higher interest rates for some mortgagors rolling off existing fixed-rate mortgages.

Most UK mortgages are held on a fixed-rate basis, with around two thirds of the stock of mortgages currently at a five-year fixed-rate period from origination. Around a third of those on fixed-rate mortgages have not re-fixed since rates started to rise in mid-2021, so the full impact of higher interest rates since then has not yet been passed through to all mortgagors. Bank staff estimates, informed by the FCA Product Sales Data, suggest that just under half of mortgages are likely to see payment increases between December 2024 and 2028.

Interest rates for those on variable rate mortgages have fallen back from their peaks. A growing number of those who are already paying higher rates may be able to refinance at a lower rate over the next two years. Just over a quarter of mortgage accounts are expected to see monthly payments decrease between December 2024 and 2028 Q1.

Monthly mortgage approvals for house purchase have risen notably since the start of 2023 and are now slightly above their 2012–2019 average. The recovery, in part, reflects declines in the average rate paid on new mortgages since quoted rates peaked in mid-2023. Banks responding to the 2024 Q4 Credit Conditions Survey also reported increased availability of secured lending to households, which was expected to continue into 2025 Q1.

In line with the recovery in housing market activity, nominal house prices have continued to pick up. The official ONS UK HPI measure rose by 3.0% in the three months to November compared with the same period a year ago. The recovery in house prices partly reflects past interest rate rises providing less of a drag.

The rate of decline in construction output compared to a year ago continues to ease. Positive output growth is now expected to return during 2025 H2; but weaker confidence following the Budget and supply constraints suggest it will be modest.

Private housebuilding rates continue to pick up. Repair and maintenance output is up modestly on a year ago, spend on commercial renovations has improved and social housing providers are focusing on improving existing stock, but fewer households are undertaking housing renovations. New commercial development remains down on a year ago.

Estate agents reported slightly higher levels of sales in 2024 Q4, but overall confidence in the housing market remains fragile.

The lower end of the market appears strongest, driven by first-time buyers. Activity is expected to pick up in Q1 ahead of stamp duty increases in April, but few expect a buoyant market throughout 2025. House prices are expected to rise modestly over the course of the next 12 months.

Renting

Demand has softened in the rental market and tenants are less willing to accept further increases in rental price. Landlords are more willing to accept lower profits on rental properties to retain desirable tenants ahead of the ban on no-fault evictions.

Get in touch

We are your online mortgage broker, offering you the convenience of applying for a mortgage online. However, we understand that sometimes you may prefer to speak with a human - phone, email or in person.

- Phone number

- 01133 205 902

- hello@cyborg.finance

- Postal address

-

31 Bradford Chamber Business Park,

New Lane, Bradford, BD4 8BX

Looking for career in Mortgage Advice? View job openings.

We are authorised and regulated by the Financial Conduct Authority (No. 919921). The FCA does not regulate most Buy to Let mortgages.

Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

Cyborg Finance Limited is registered in England and Wales (No. 12131863) at Bradford Chamber, New Lane, Bradford, BD4 8BX