Financial Services

-

Home Buyer Mortgage

First Time Buyer Guide to buying your own home.

-

Home Mover Mortgage

Elevate your move with our tailored Home Mover Mortgage for a smooth transition to your new dream home.

-

Home Owner Remortgage

Refinance with our Home Owner Remortgage for better rates, releasing equity, or funding improvements—empowering your homeownership journey.

-

Buy-to-Let Mortgage

Dive into property investment with our Buy-to-Let Mortgage, tailored for both seasoned investors and first-timers seeking to build a profitable portfolio.

-

Holiday Let Mortgage

Transform your vacation home investment dreams into reality with a Holiday Let Mortgage,

-

Green Mortgages

Green Mortgages 🌳 are a new type of mortgage that rewards you for making your home more energy efficient.

-

Bad Credit

Mortgages Adverse Credit Mortgages 📉 are for people with a poor credit history.

-

Private Medical Insurance

Cut NHS wait times with private medical care and private hospitals.

-

Life Insurance

Pay off your mortgage if you or your partner die.

-

Bridging Finance

Navigate property transitions seamlessly with our Bridging Finance, offering quick and secure solutions for your short-term financial needs.

-

Auction Finance

Secure your auction triumph with Auction Finance, providing the financial backing needed to confidently bid and acquire your desired property.

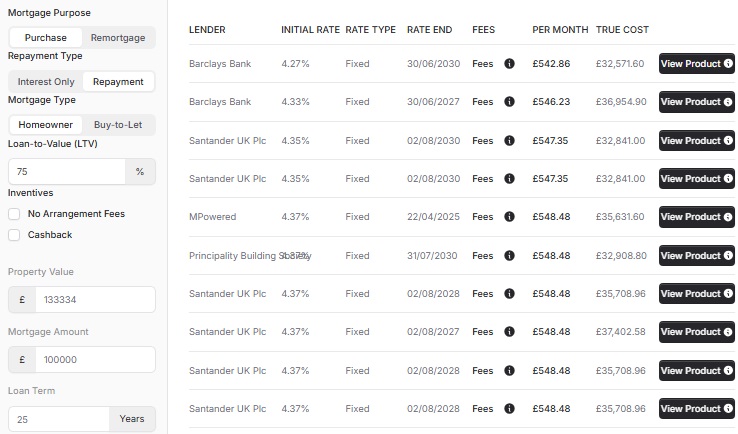

How much can I borrow? | Buy-to-Let Mortgage Calculator

Buy-to-Let mortgage affordability is calculated based on the rent a property achieves. The greater the rent, the higher the loan amount you can borrow.

How to calculate buy-to-let mortgage affordability?

Buy-to-Let mortgage affordability is calculated based on the rent a property achieves. The greater the rent, the higher the loan amount you can borrow.

A rental stress test formula determines the maximum mortgage.

Except, there is also maximum loan-to-value—typically 85% of the value of the property.

What is the rental stress test formula?

Mortgage Lenders have different criteria, but we can work estimate from the averages.

On standard buy-to-let, your rent must is 125% higher than your mortgage payments at a payment rate of 5.5%.

Given £500 rent the formula would be:

£500 (times) 12 (divide) 125% (divide) 5.5%

On a calculator:

£500*12/1.25/0.05 = £96,000

Higher Rate Taxpayers use an increased rental formula of 145% up from the standard 125%. The use of a Limited Company (SPV) can lower it back down to the standard.

Houses in Multiple Occupation (HMO) also use an increased rental formula of 145% up from the standard 125%.

Remortgaging is exempt from the regulation, but lenders implement the stress test as standard good practice.

Note: These stress tests were introduced in January 2017 by the Prudential Regulation Authority (PRA)

I'm just below affordability, what can I do?

Talk to our mortgage advisers about a rental stress test top-up. Some mortgage lenders will take your income into account as well as the rental income.

How is buy-to-let mortgage cost calculated?

The mortgage calculator only calculates the interest-only payment. If you want a repayment mortgage, the monthly cost will be higher.

Given £50,000 mortgage and interest at 2.5% the formula would be:

£50,000 (times) 2.5% (divide) 12

On a calculator:

50000 * 0.025 / 12 = £104

You can lower the mortgage costs by obtaining a mortgage with a lower interest rate. Otherwise, put a higher deposit into the property lowering the loan required.

What is Rental Yield Calculation?

Landlords use rental yield as a metric to calculate the value of the property investment. It allows the natural side by side comparison of properties.

How is the rental yield calculated?

On this mortgage calculator, we use Gross Rental Yield using only property value and rent. Net Rental Yield also includes costs and maintenance.

Given £100,000 property and rent of £500 the formula would be:

£500 (multiply) 12 (divide) £100,000 * 100

On a calculator:

500 * 12 / 5000 * 100 = 6%

There is no set rule for minimum rental yield, but our professional landlords tell us they aim for 7% or higher.

What is the Loan to Value (LTV) Calculation?

Loan to Value (LTV) is used to express how much of the property value will be mortgaged.

A 70% LTV Mortgage on the house valued at £100,000 will have a £70,000 mortgage and £30,000 deposit.

The formula for Loan to Value (LTV) is:

£70,000 (divide) £100,000 (times) 100

On a calculator:

70000 / 100000 * 100 = 70%

Use our Loan-to-Value Calculator to find out your LTV.

-

Loan To Value (LTV) Calculator

>

Calculate your LTV for a mortgage, you need to know (or estimate) the value of the property and the mortgage amount.

-

Mortgage Overpayment Calculator

>

Calculate the effects of overpaying your mortgage

-

Buy-to-Let Maximum Loan Calculator

>

Calculate the maximum Buy-to-Let Loan from your acheiveable rent.

Get in touch

We are your online mortgage broker, offering you the convenience of applying for a mortgage online. However, we understand that sometimes you may prefer to speak with a human - phone, email or in person.

- Phone number

- 01133 205 902

- hello@cyborg.finance

- Postal address

-

31 Bradford Chamber Business Park,

New Lane, Bradford, BD4 8BX

Looking for career in Mortgage Advice? View job openings.

We are authorised and regulated by the Financial Conduct Authority (No. 919921). The FCA does not regulate most Buy to Let mortgages.

Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

Cyborg Finance Limited is registered in England and Wales (No. 12131863) at Bradford Chamber, New Lane, Bradford, BD4 8BX